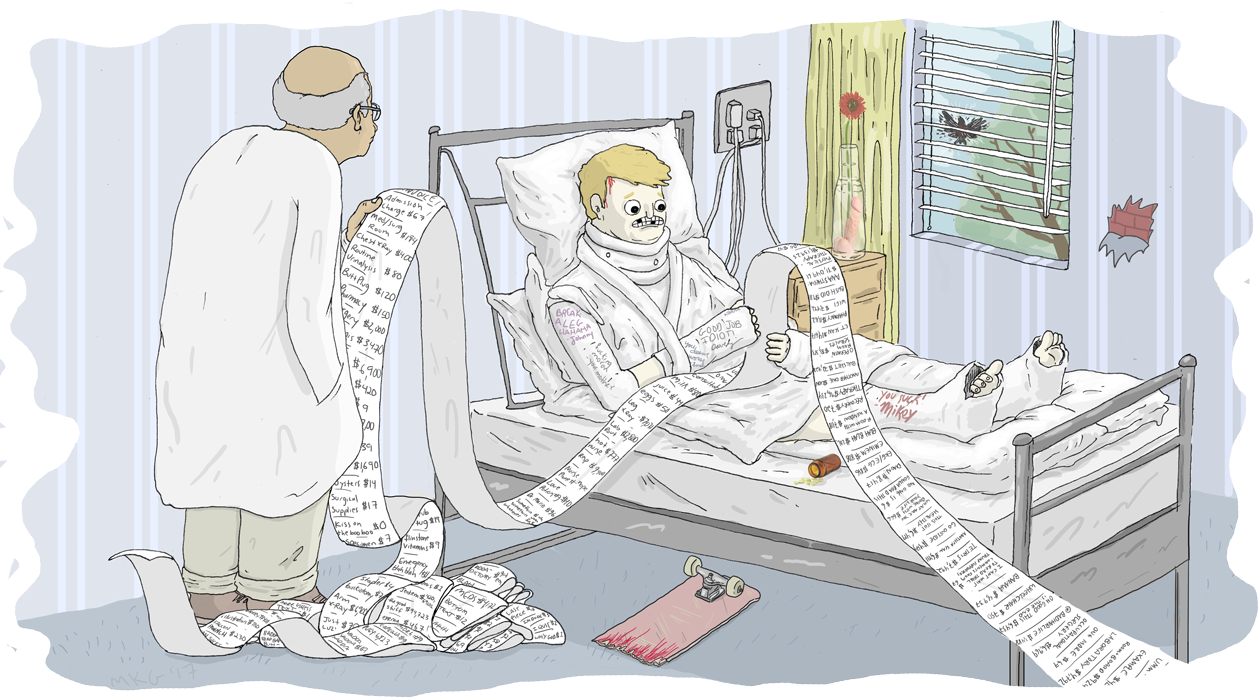

Fred Gall took a rough slam last summer in Copenhagen. He went to a hospital stateside a few days later after coughing up blood, and was handed a diagnosis of broken ribs and an $18,000 bill. “I didn’t have insurance then,” he explained, “but I don’t sweat hospital bills. When they come in the mail, I don’t even read them, I just rip them up. I have hospital bills from Miami, Las Vegas, Philly, Jersey, and I guess New York.” He said Chris Carter from Alien Workshop had covered two hospital bills in the past, but that was the closest he has ever gotten to getting health insurance from a sponsor.

It’s easy for us to become desensitized to skating’s physical dangers. We stomp tricks primo or slip out on landings but rarely bail down five stairs, let alone feel the cumulative damage of repeatedly skating and falling down big shit. The role of a pro is predicated in large part on their willingness to risk their health, but historically the industry hasn’t offered much to maintain it.

Pro skaters are just one of the many groups in the US that don’t get health insurance from their jobs though, the American health care system is infamously inefficient and expensive. And although The Patient Protection and Affordable Care Act (also known as Obamacare or the ACA) was signed into law in 2010, these problems have persisted. Now, with the GOP talking about taking another go at repealing and replacing Obamacare, it’s worth looking at how the skate industry has dealt with the issue of health insurance so we know where we’re currently at and where we need to go.

The first step in looking at how Obamacare impacted the skate industry is understanding how it’s structured. Going back to Fred Gall, the reason he was never offered health insurance isn’t because the cost of covering him would drive a company into bankruptcy, it’s because he was never an employee of any of his sponsors.

Legally, pro skaters and the golfers in the PGA are both independent contractors getting the same style of endorsement deals. Rather than offering a skater full-time employment and having to pay for the benefits and payroll taxes that go along with it, skaters sign a contract that exchanges money for a service: “If so and so skates our stuff and gets coverage doing so, we will pay them this much money.” The practice isn’t limited to pros, and artists making board graphics, filmers and sales reps are often freelancers too. Full-time employees might get benefits like a 401k or insurance—the ACA requires any business with over 50 employees to offer a healthcare plan—but freelancers are on their own.

joey brezinski / photo: mehring

It’s not unheard of for a sponsor to help a pro with medical bills, and for big corporate sponsors to offer even more. Joey Brezinski explained to me that Red Bull Headquarters houses a physical training facility where their skaters (and other sponsored athletes) have access to a gym and physical therapists to strengthen and bounce back from injuries. “That’s the best, as far as all sponsors,” he said. “They actually want us to recover quicker if we do have an injury and provide what we need to do that.” They don’t offer health insurance though, and Brezinski told me that he pays close to $600 a month for coverage, which he got through a broker.

As far as I can tell, not offering insurance is the industry standard. “I mean maybe there are some exceptions, like if you’re Rick Howard and own Girl,” Lee Berman, the team manager for Cons told me. “But I don’t know any pro skateboarders that get health insurance through any of the companies they skate for.” He said some Cons riders don’t have coverage, others are still covered under their parent’s plan (which the ACA allows until someone turns 26 or gets married), and a lot of them buy private health insurance.

One of the most recognizable parts of the ACA is the individual mandate, meaning that everyone has to either get insurance from an employer’s plan or buy one directly from an insurance company. The federal government, which provides Medicaid insurance for people in poverty, also pledged to subsidize plans to bring costs down for people just outside of eligibility for Medicaid.

The subsidies weren’t available to Kevin Coakley when he tried to apply for insurance this year. “My friend actually signed up and he went through the process and somehow got his health insurance down to something crazy. It was like $40 or $50 a month. And I was like if he can get it down to that, I must be able to too. So I applied, and he even helped me, but for some reason, mine came out to being like, fucking $500 a month” Coakley went back and applied saying that he made less money but still couldn’t get it under $350 a month. “It’s just too expensive, I can’t commit to paying hundreds of dollars a month to have this plan that I feel as though, knock on wood, I’m barely gonna use or never gonna use.”

arto, photo: ed templeton

The Kalis family didn’t get subsidies either. Before the law went into effect, Josh said he was buying coverage for his family that would have covered major medical events: “Let’s say I broke my leg or my daughter got sick and we had to get her checked out and get a prescription. If it was below 5,000 bucks we didn’t to pay for it.”

But the ACA established a higher standard of insurance coverage, saying that all plans needed to have essential health benefits similar to what a typical plan offered by an employer would have. “I had to readjust my health care coverage to meet these new minimums,” he said. “Now I have to have maternity, I have to have prescription coverage. I have to pay for all this bullshit that my family don’t use. All we really cared about was if anything major happened with hospital stays or surgeries. So my healthcare went from $340 a month to $1,200 a month.”

Having a monthly bill triple, not surprisingly, made it harder for him to budget. “Maybe some shit goes down at DC or Kayo or whatever it is that affects me and I have to take less pay for a few months so they can do some other things or whatever,” he said. “I don’t have a problem with that shit, so I agree to it. However, my health care coverage stays the same. So there’s a big difference if you’re bringing in 10 g’s a month and your insurance is $1,300 versus if you’re bringing in 5 g’s a month and your health coverage is $1,300.” Eventually, he was forced to skip an insurance payment. “I immediately got taken off. So now I’ve got no health care for me and my family. But guess what? They throw a fine on you. And they say that they won’t come after you for that fine unless you get a W2 and they’ll take it out of your tax refund. Well, I don’t get W2s, I get 1099s. So for every month we don’t have health care, we get fined.”

injured ed, photo: deanna

Tum Yeto [distributors of Toy Machine, Pig, Foundation..etc] has never offered skaters coverage but encourages them to get insured one way or another. They supplemented riders coverage in the past, offering money to cover additional medical expenses not covered under their existing plan. “They would get a policy and they would be covered 80% and we would cover the 20%,” Mike Sinclair [Tum Yeto TM] explained. “Riders started letting their policy lapse and they weren’t using the extra percentage for insurance. So it was like, we’re not paying this anymore and the budgets just didn’t allow it. Which sucks but it just wasn’t working out.” Still, he tries to impart the importance of being covered and prepared in the event that something goes wrong.

“Any new team rider, or up and coming kid that I have, I’m just like, make sure you have insurance. Anything can happen,” he said. “I blew my knee out on the simplest thing. Skateboarding is so weird and you can’t guess when you’re going to get hurt. I don’t think a lot of people think about it until they get hurt.”

As skaters get older, insurance becomes more of a necessity. Some start families, others start to feel the tide of aging, and sometimes medical situations come up that have nothing to do with skating. Dan Drehobl started rapidly losing weight in 2012 and assumed it was because he had quit drinking. A few pounds turned into 30 and he started noticing that he didn’t feel right, so he sought out a medical opinion. “Probably the most noticeable symptom was that I never had any energy,” he said in an email. “I would try to go skating all the time and end up just taking a nap in the grass instead. I went to numerous doctors to try to figure out what was wrong with me and none of them could figure it out. I was convinced that I had Chronic Fatigue Syndrome.”

It turned out to be Type 1 Diabetes, an autoimmune disease that’s genetically inherited. It requires lifelong care and multiple prescriptions, and neither are cheap. Part of the ACA is a law that says insurers can’t charge Drehobl higher rates of coverage or refuse him because of his pre-existing condition, which ensures his access to care at affordable rates. “Currently I am receiving all the treatment and care that I need but I’m not sure how long that will last,” he wrote. “With a president who has promised to repeal the Affordable Care Act and a congress who has already taken steps to defund it I am really fearful of my future.”

He also mentioned being worried that the provisions that prevent insurance companies from denying coverage would be gone. If that’s the case it’s not just diabetic skaters that should be worried. A blown ACL being replaced isn’t a disease, but it’s going to show up on medical records. Insurance companies make money by taking in enough in premiums to make a profit after paying for the treatment of the people covered by the plan. A skater who has had major surgery could be deemed a higher risk of having costly medical bills in the future than an office worker. Right now they’d pay the same price for the same health plan, but if the laws change, more pros could be forced to roll the dice and skate without coverage.

fred gall roll in / photo: xeno tsarnas

Even if companies offered insurance, Fred Gall might not be getting benefits in the twilight of his career. “It just sucks at the end when they let you go,” he said. “I still have a board, but I get paid dick.” He supplements that income by working as a set builder, a tried and true New York City skate job. He was getting free coverage through the ACA for a while, but lapsed and is struggling to re-enroll. “I’ve been trying to renew it since about June, and they want 3-months of pay stubs and blah blah blah,” he said. “I brought them all the information, and they say they’re gonna get back to me and then they don’t. Then I call them a bunch of times and they give me the fucking run around. And then I just stopped caring for a couple months. Then I get a letter in the mail that they’re gonna fine me $1,700. So anyways, I’m still working on getting Obamacare.”

With Paul Ryan conceding that the law would be around for the foreseeable future and President Trump promising that it’ll explode, the future remains unclear. Updates to the law are scheduled to continue to roll out until 2022, so even if it survives any future attacks we won’t have a complete picture of its effect for a while. It doesn’t seem like much of a stretch to say that Fred’s situation is emblematic of the law: sometimes it hits the mark of providing affordable coverage, but other times it’s weighed down by bureaucratic red tape.

Ultimately the law may roll out as planned, or it could be gutted, but skateboarders will keep skating either way. We can just hope they’ll be able to afford to get hurt.

Related Posts

-

STOP WATCHING SKATE VIDEOS

STOP WATCHING SKATE VIDEOS

You heard the man!

-

IS ZUMIEZ GOOD FOR THE SKATE INDUSTRY?

IS ZUMIEZ GOOD FOR THE SKATE INDUSTRY?

An honest look at one of the most taboo questions in skateboarding today.

-

WE (SERIOUSLY) WATCHED TODD FALCON’S INDIE SKATE HORROR FILM

WE (SERIOUSLY) WATCHED TODD FALCON’S INDIE SKATE HORROR FILM

We wrote a semi-serious review of the Original Skateboard Freak's newest indie film.

-

DIVING INTO VANS “CREDITS” AND THE VIDEOS THAT PAVED THE WAY

DIVING INTO VANS “CREDITS” AND THE VIDEOS THAT PAVED THE WAY

The recent push is a sign that brands are beginning to understand how to foster actual growth and energize the community.

-

HOW “BAKER 3” BANGED US OVER THE HEAD

HOW “BAKER 3” BANGED US OVER THE HEAD

We overanalyzed the most straightforward skate video of the 2000s.

-

FINDING EASTER EGGS IN TOM KNOX’S NEW ATLANTIC DRIFT PART

FINDING EASTER EGGS IN TOM KNOX’S NEW ATLANTIC DRIFT PART

Peep some of the little secrets and tributes that Tom Knox and Jacob Harris baked into their newest video.

-

HOW TO MAKE MONEY FILMING SKATEBOARDING

HOW TO MAKE MONEY FILMING SKATEBOARDING

Hear from three full-time filmers on how to price, sell, and protect your precious clips.

-

HOW TWO SHOPS ARE WORKING TOGETHER TO MAKE IT THROUGH THE PANDEMIC

HOW TWO SHOPS ARE WORKING TOGETHER TO MAKE IT THROUGH THE PANDEMIC

Two skateshops, one deck.

Comments

Popular

-

A CHAT WITH LUDVIG HAKANSSON, THE OLDEST SOUL IN SKATEBOARDING

A CHAT WITH LUDVIG HAKANSSON, THE OLDEST SOUL IN SKATEBOARDING

The man loves to read Nietzche, skates in some expensive vintage gear, and paints in his own neoclassical-meets-abstract-expressionist style.

-

HANGING OUT WITH ANDREW HUBERMAN, SKATEBOARDER TURNED NEUROSCIENTIST

HANGING OUT WITH ANDREW HUBERMAN, SKATEBOARDER TURNED NEUROSCIENTIST

Curious what it would be like to hang with this guy outside of a stuffy podcast studio? Us too.

-

GROWING UP, MOVING OUT, AND BREAKING BOARDS

GROWING UP, MOVING OUT, AND BREAKING BOARDS

A personal essay recounting a love affair with something we're all too familiar with.

-

INTRODUCING THE NEW JENKEM COLLECTION, JUST IN TIME FOR THE HOLIDAYS

INTRODUCING THE NEW JENKEM COLLECTION, JUST IN TIME FOR THE HOLIDAYS

Air fresheners, bumper stickers, a shirt with a gun on it and a bunch of other stuff.

-

HOW CHAD CARUSO SKATED ACROSS AMERICA

HOW CHAD CARUSO SKATED ACROSS AMERICA

Chad did it the way most skateboarders would: independently and without much of a plan.

June 26, 2017 11:02 am

As a Finn i’v allways wondered how it works for adults who arent covered by their parents.. Cause we never had to even think about ‘can my family afford healthcare’ stay strong you US lifers!!!

June 26, 2017 11:42 am

Sounds like the Visual Effects and the movie industry, and the majority of jobs in California… taking over the whole country… hire somebody for the duration of the job, and dismiss when completed. No benefits or stability.

Companies should be forced to hire people full-time.

June 30, 2017 9:18 pm

I’m an older skater who was never talented enough to make it in the industry. So I went to college and got a degree in Public Health. After college I started working for a community health center and became a Certified Application Counselor. We help people get enrolled in healthcare through the ACA. Explain deductibles, co-insurance, out of pocket maxes…etc. your monthly payment is all determined based upon a persons income. If you are self employed you need to keep up with changes to your income quarterly. When you do an application you are projecting your income for the next year. Based upon what you estimate on your application is how your monthly premium is determined. The higher the income the more a premium is going to be. If you claim a dependent it will lower the premium. If you are married it counts all household income. Picking a plan is all determined on how much you are going to use it and what services you need. If you go to the doctor often or need therapy, or you see a specialist, these are all things that need to go into making a decesion on what kind of coverage to get. Go see a CAC, Navigator, or Broker they will help you decide how to file and what to choose. A lot of these services are free and available at local health clinics. You can find how to locate one near you on healthcare.gov and also see plans and prices on the screener page to determine what you’ll pay. Hope his helps and keep shredding.

July 2, 2017 4:47 am

Thank god for the NHS, I spent 3 weeks in hospital 2 years ago for a spiral fracture through both Tib and Fib, had an external fixate on it then a rod and bolts in put in. Then last month had it removed, and spent a week in hospital for treating an infection from the initial op, now on antibiotics for treating the infection and guess what, it’s free all due to the NHS. I think I would be bankrupt if I was in the states.